China’s luxury market has long been the envy of the world. With a growth rate of 30% in 2011, it seemed a pretty safe bet that the positive trajectory would continue unabated long into the future. Against the odds, however, 2013 actually saw a slowing of the market to 2% with a number of high profile brands including Giorgio Armani, Dolce & Gabbana and Patek Philippe closing their flagship stores in The Bund1 in Shanghai.

These high profile closures could simply be representative of a change in retail location or amended lease terms, but when you look at the growth trend in the last three years – the luxury sector grew 30% in 2011, 7% in 2012 and 2% in 2013 – it is unsurprising that luxury brands are reviewing their strategy in China.

In early 2013, LVMH (Louis Vuitton – Moët Hennessy) Group announced that they will cease immediate expansion in second and third tier Chinese cities.

Does this mean that the party is finally over for luxury brands in China?

To provide a fair judgment on what lies ahead for Chinese luxury market, we first need to look at the reasons behind the recent slowdown in growth:

The luxury sector grew 30% in 2011, 7% in 2012 and 2% in 2013.

1. The Ban on Luxury Gift Giving

In June 2012, the Chinese Central Government brought in new rules to

prevent official expenses being used for the purchase of luxury items.

According to the ‘Hurun Report’ / ‘Hurun Chinese Luxury Customer Survey (2014)’2, this anti-corruption drive is already having an impact, with a 25% drop in luxury gift giving during 2013. Western luxury brands like Louis Vuitton, Chanel and Cartier aren’t the only brands feeling the effects of these new rules; Chinese luxury rice wine brand, Maotai, has also seen a 40% drop in sales.

2. Overseas Spending

Luxury items can cost up to twice as much in China as they might in Europe or North America. In China, high end luxury goods are subject to significant rates of tax, whereas VAT reclaims on goods bought overseas lowers the purchase cost significantly. A simplified visa application3 process in the Schengen regions, coupled with measures implemented by the British Government, means that wealthy Chinese now largely prefer to spend overseas. A handbag that costs £4,000 in China would cost around £2,000 in London, with the savings on one item alone more than covering the cost of the trip.

The differential on big ticket items such as watches, jewellery or bespoke designer clothes can be even greater. According to Bain & Co’s Report ‘China Luxury Goods Market Study 2013’, over 60% of luxury purchases now take place outside China. This compares with 2005 when a mere 5% of Chinese consumers spent outside their home country.

“Over 60% of luxury purchases now take place outside China. This compares with 2005 when a mere 5% of Chinese consumers spent outside their home country.”

3. Changing Behaviour

The last decade has seen China develop into the world’s second largest economy with a corresponding increase in confidence among Chinese consumers. Previously, affluent Chinese often displayed their wealth by purchasing luxury items with big brand logos or by showing off their ‘bling’. Nowadays, wealthy individuals prefer to demonstrate their individuality with items that are rare and exclusive, rather than simply expensive.

Following the Beijing Olympics, China was frequently cited as an ‘economic superpower’ by many countries, including the UK, that were looking to attract Chinese investments. However, it must be remembered that China is still, by and large, a developing country. Looking beyond first and second tier cities it is still relatively easy to find scenes of poverty.

As a result of this uneven distribution of wealth, prosperous individuals are increasingly reluctant to draw attention to themselves.

Further, there has been a corresponding shift in priorities amongst those individuals, away from personal ‘bling’ to more global concerns.

Wealthy Chinese are now realising that the economic boom of the last few decades has caused severe air pollution and damage to the environment. If the pollution level continues to rise, Chinese people will have no choice but to watch the sun set over a large screen, as happened in Tiananmen Square in Beijing during early 2014.4 The impact of environmental damage on their own health, and the health of their children, is taking precedence over spending on luxury goods. This is a trend that looks set to continue.

Sunset on screen in Tiananmen Square.

“Personal shoppers usually receive a commission of between 10-15% of the purchase price in Europe, whilst their clients in China benefit from a 30-40% discount compared with what they would usually pay.”

4. The Rise of ‘Daigou’ Personal Shoppers

Personal shopping is a growing phenomenon in China. International students, flight attendants and tourists are building micro businesses to offer substantial deals for domestic customers; deals made possible by capitalising on the price differential.

Chinese social media platforms such as Weibo, WeChat and QQ include hundreds, if not thousands, of personal shoppers – known as ‘Daigou’ – promoting luxury items for sale online.

More recently, following a number of food safety scandals in China, Daigou are also using their sites to sell other high margin items such as baby milk powder5 and medicines.

5. Fake Branded Products

The relationship between fake and genuine goods has gone through a number of twists and turns in recent years. Many Chinese people believed that fake goods contributed to the rising popularity of the brand. Most luxury brands in China, such as Louis Vuitton, have taken stringent measures to crack down on fake products in order to protect their Intellectual Property. However, even at a time when wealthy Chinese liked to show off big brand logos, the desire to own the ‘genuine article’ never faded as a representation of status.

Times have changed and as cited by the Hurun Report, Louis Vuitton has, for the first time, lost its crown as the preferred brand for luxury gifts in China. Popular designs that attract fake products are now seen as ‘uncool’ in China and this has become an increasingly challenging area of product development for brands.

“The desire to own the ‘genuine article’ never faded as a representation of status.”

Popular designs that attract fake products are now seen as ‘uncool’ in China.

So Where Are The Opportunities?

This subdued analysis might call into question the potential of the Chinese market for new international brands.

Dig a little deeper, however, and the future is actually full of opportunities.

A New Affordable Luxury

During this ‘cooling-off’ in the growth of the luxury market in China, a number of ‘affordable luxury’ brands have seen dramatic growth.

American brand Coach, for example, reported 40% growth in China in 2013 having positioned itself in this category. According to a QQ Finance6 analysis of Chinese media, Coach is successfully pitching itself as a brand that many Chinese consumers either use themselves or buy for family and friends. It doesn’t hurt that compared to many European brands, Coach products are usually 40-60% cheaper.

“The Premium market, with premium referring to ‘affordable luxury’, is where the big numbers are going to be.”

Fuelled by such growth, Coach is likely to continue expanding beyond its 49 stores in China and focus on opening in second and third tier Chinese cities.

The affordable luxury sector in China is also witnessing the emergence of new indie labels7 targeting a number of specific niche crowds. This is positive news for British designers and brands who would otherwise struggle to compete on the same level as major international brands. This shift in customer preference represents huge opportunities for British brands, whether they are fashion designers in London or whisky distilleries in the Lake District. Multi-brand boutiques or lifestyle stores also offer a perfect match for these smaller, niche outlets.

Furla, an Italian accessories brand that targets the affordable luxury market, is already exploiting these opportunities. In a recent interview,8 the company’s CEO, Eraldo Potello, said: “The Premium market, with premium referring to ‘affordable luxury’, is where the big numbers are going to be. It’s not just because the Government is discouraging extravagant spending. People tend to want value for money and great, authentic products at affordable price points.”

Exclusivity VS Accessibility

One of the challenges faced by luxury brands in China is in finding the perfect position between exclusivity and accessibility.

Whereas brands such as Coach have found it profitable to operate within the ‘affordable luxury’ bracket, some brands have taken the decision to define themselves at the other end of the scale.

One such example is luxury travel agent, Affinity China, which provides unique travel experiences for wealthy Chinese. Dubbed by Forbes as ‘post-luxury luxury’ and Marketing Magazine as ‘extreme luxury’, Affinity China and similar brands are aiming at the exclusive elite.

As the Chinese luxury market gets more sophisticated, opportunities for brands that have a truly unique brand proposition can only increase.

Monaco, one of the favourite holiday destinations for the Chinese super wealthy.

Embracing Pop-up

Decades of economic boom have meant that the cost of bricks and mortar is becoming prohibitively high for many new brands targeting tier one and tier two Chinese cities.

Despite huge financial commitments, brands entering China still face barriers when it comes to understanding politics, liaising with landlords, and responding to regional differences in customer preferences and marketing channels. This makes it far more difficult to open a retail store than it was just a few years ago.

Many forward thinking brands and retailers are embracing new ways of launching their brands in China.

One of the most successful examples is British fashion retailer Topshop, who experimented with a single outlet in Shenzhen before opening 30 pop-up stores all over China.9 If you understand the notoriously disparate Chinese market, you’ll understand that’s a smart move.

On any given day, it can be snowing in northern China, whilst people in the south might be wearing a short-sleeved shirt. Tastes, sizes and buying habits all vary enormously across China, with no two provinces behaving the same.

Topshop’s pop-up strategy allowed them to gain a clear understanding of customer needs before making a bricks and mortar investment. It also enabled the brand to establish relationships with landlords, press and media, whilst reinforcing Topshop’s style driven image – a highly appealing proposition for Chinese consumers.

The pop-up approach also works well for luxury brands who want to launch limited edition capsule collections. Fashion house Dior promoted Raf Simon’s first collection through a pop-up store, which opened for just one month in Beijing.

Brands operating in China are already familiar with running exhibitions or promotions in shopping malls, as this offers an excellent way to connect with real customers. With the right planning, it can be an extremely cost effective way to launch or test a brand in China.

Engage Digitally

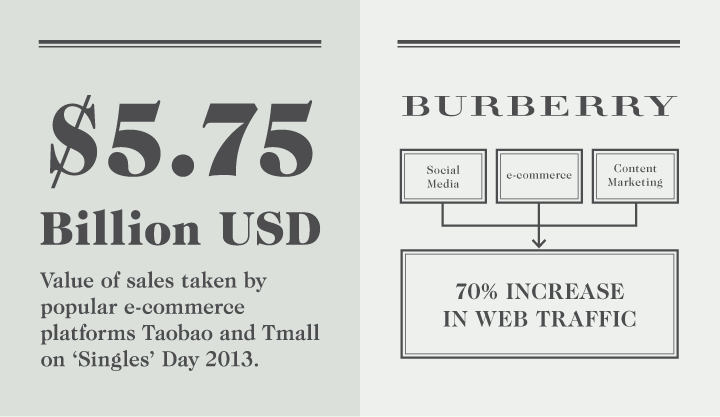

November 11 is ‘Singles’ Day’ in China – a day of celebration for all people who are single. In 2013, Taobao and Tmall, two of China’s most popular e-commerce platforms, took 5.75 billion USD10 of sales on this day.

The huge potential of e-commerce platforms is forcing all brands, luxury or not, to invest in their digital strategy.

Coupled with this, the next generation of luxury consumers11 typically defined as the ‘post-90s’ demographic, have grown up with mobile. As a result, it’s little surprise that buying online is becoming the norm in China.

Burberry’s comprehensive digital strategy12 combining social, e-commerce and content marketing, is cited as a prime example for other brands: having resulted in a 70% increase in traffic to their website and 400,000 fans on Weibo.

Relationship With Customers

Chinese consumers are well known for being less tolerant of mistakes from western brands than Chinese brands. That is why developing a good relationship with consumers is vitally important for all brands looking to tap into the Chinese market.

After a hiccup in customer service last year, Apple’s CEO issued a direct apology to Chinese consumers whilst in 2012, the boss of French boutique hotel Zadig and Voltaire (by the fashion label Zadig and Voltaire) was forced to apologise after saying that they intended to ban Chinese tourists. In both instances, the sentiments went viral via social media with both the public and influential bloggers recommending a boycott of each brand.

Developing a good relationship with Chinese consumers is not dissimilar to the relationship a brand would seek to develop in any other country. The most important thing to remember is to treat customers well, treat them with respect and make them feel special.

Conclusion

2014 will see China’s luxury sector enter a new era. As Chinese consumers become more sophisticated, their desire for stand-out brands across different price points will only increase.

The slowdown in growth has already created winners like Coach or Furla, but for new brands targeting China this is a very interesting time to enter the market.

There is no denying China’s competitiveness, but the potential in many second and third tier cities remains largely untapped. New brands should learn from the experiences of key international brands who have entered the Chinese market in the last decade. There are many great examples of brands that have successfully launched in China, but similarly there many examples of brands that have been less than successful in their approaches.

The Chinese market is definitely hungry for the right proposition – is your brand ready for it in 2014?

“As Chinese consumers become more sophisticated, their desire for stand-out brands across different price points will only increase.”

To see how UKC Company can help you reach China, please contact our China team [email protected]

References

- Want China Times – Foreign Luxury Brands Desert Shanghai’s Bund as Glamor Fades

- Hurun Report – Hurun Report Chinese Luxury Consumer Survey 2014

- Financial Times – UK Visa Rules Deter Chinese Shoppers

- Daily Mail – China starts televising the sunrise on giant TV screens because Beijing is so clouded in smog

- The Guardian – Baby Milk Powder Rationing Introduced by Supermarkets

- QQ Finance – 奢侈品在中国大衰退:最容易赚钱时代已过去

- Jing Daily – 3 Trends That Show it’s the Right Time for Indie Labels in China

- South China Morning Post – Furla weaves China dream amid affordable luxury boom

- South China Morning Post – Topshop sets sights on ‘pop-up’ campaign

- Bloomberg – Alibaba Breaks Sales Record Amid China Singles-Day Rebate

- UKC Company – The Young Yuan

- Jing Daily – What Burberry Is Doing Right In China

China’s luxury market has long been the envy of the world. With a growth rate of 30% in 2011, it seemed a pretty safe bet that the positive trajectory would continue unabated long into the future. Against the odds, however, 2013 actually saw a slowing of the market to 2% with a number of high profile brands including Giorgio Armani, Dolce & Gabbana and Patek Philippe closing their flagship stores in The Bund1 in Shanghai.

These high profile closures could simply be representative of a change in retail location or amended lease terms, but when you look at the growth trend in the last three years – the luxury sector grew 30% in 2011, 7% in 2012 and 2% in 2013 – it is unsurprising that luxury brands are reviewing their strategy in China.

In early 2013, LVMH (Louis Vuitton – Moët Hennessy) Group announced that they will cease immediate expansion in second and third tier Chinese cities.

Does this mean that the party is finally over for luxury brands in China?

To provide a fair judgment on what lies ahead for Chinese luxury market, we first need to look at the reasons behind the recent slowdown in growth:

The luxury sector grew 30% in 2011, 7% in 2012 and 2% in 2013.

1. The Ban on Luxury Gift Giving

In June 2012, the Chinese Central Government brought in new rules to

prevent official expenses being used for the purchase of luxury items.

According to the ‘Hurun Report’ / ‘Hurun Chinese Luxury Customer Survey (2014)’2, this anti-corruption drive is already having an impact, with a 25% drop in luxury gift giving during 2013. Western luxury brands like Louis Vuitton, Chanel and Cartier aren’t the only brands feeling the effects of these new rules; Chinese luxury rice wine brand, Maotai, has also seen a 40% drop in sales.

2. Overseas Spending

Luxury items can cost up to twice as much in China as they might in Europe or North America. In China, high end luxury goods are subject to significant rates of tax, whereas VAT reclaims on goods bought overseas lowers the purchase cost significantly. A simplified visa application3 process in the Schengen regions, coupled with measures implemented by the British Government, means that wealthy Chinese now largely prefer to spend overseas. A handbag that costs £4,000 in China would cost around £2,000 in London, with the savings on one item alone more than covering the cost of the trip.

The differential on big ticket items such as watches, jewellery or bespoke designer clothes can be even greater. According to Bain & Co’s Report ‘China Luxury Goods Market Study 2013’, over 60% of luxury purchases now take place outside China. This compares with 2005 when a mere 5% of Chinese consumers spent outside their home country.

“Over 60% of luxury purchases now take place outside China. This compares with 2005 when a mere 5% of Chinese consumers spent outside their home country.”

3. Changing Behaviour

The last decade has seen China develop into the world’s second largest economy with a corresponding increase in confidence among Chinese consumers. Previously, affluent Chinese often displayed their wealth by purchasing luxury items with big brand logos or by showing off their ‘bling’. Nowadays, wealthy individuals prefer to demonstrate their individuality with items that are rare and exclusive, rather than simply expensive.

Following the Beijing Olympics, China was frequently cited as an ‘economic superpower’ by many countries, including the UK, that were looking to attract Chinese investments. However, it must be remembered that China is still, by and large, a developing country. Looking beyond first and second tier cities it is still relatively easy to find scenes of poverty.

As a result of this uneven distribution of wealth, prosperous individuals are increasingly reluctant to draw attention to themselves.

Further, there has been a corresponding shift in priorities amongst those individuals, away from personal ‘bling’ to more global concerns.

Wealthy Chinese are now realising that the economic boom of the last few decades has caused severe air pollution and damage to the environment. If the pollution level continues to rise, Chinese people will have no choice but to watch the sun set over a large screen, as happened in Tiananmen Square in Beijing during early 2014.4 The impact of environmental damage on their own health, and the health of their children, is taking precedence over spending on luxury goods. This is a trend that looks set to continue.

Sunset on screen in Tiananmen Square.

“Personal shoppers usually receive a commission of between 10-15% of the purchase price in Europe, whilst their clients in China benefit from a 30-40% discount compared with what they would usually pay.”

4. The Rise of ‘Daigou’ Personal Shoppers

Personal shopping is a growing phenomenon in China. International students, flight attendants and tourists are building micro businesses to offer substantial deals for domestic customers; deals made possible by capitalising on the price differential.

Chinese social media platforms such as Weibo, WeChat and QQ include hundreds, if not thousands, of personal shoppers – known as ‘Daigou’ – promoting luxury items for sale online.

More recently, following a number of food safety scandals in China, Daigou are also using their sites to sell other high margin items such as baby milk powder5 and medicines.

5. Fake Branded Products

The relationship between fake and genuine goods has gone through a number of twists and turns in recent years. Many Chinese people believed that fake goods contributed to the rising popularity of the brand. Most luxury brands in China, such as Louis Vuitton, have taken stringent measures to crack down on fake products in order to protect their Intellectual Property. However, even at a time when wealthy Chinese liked to show off big brand logos, the desire to own the ‘genuine article’ never faded as a representation of status.

Times have changed and as cited by the Hurun Report, Louis Vuitton has, for the first time, lost its crown as the preferred brand for luxury gifts in China. Popular designs that attract fake products are now seen as ‘uncool’ in China and this has become an increasingly challenging area of product development for brands.

“The desire to own the ‘genuine article’ never faded as a representation of status.”

Popular designs that attract fake products are now seen as ‘uncool’ in China.

So Where Are The Opportunities?

This subdued analysis might call into question the potential of the Chinese market for new international brands.

Dig a little deeper, however, and the future is actually full of opportunities.

A New Affordable Luxury

During this ‘cooling-off’ in the growth of the luxury market in China, a number of ‘affordable luxury’ brands have seen dramatic growth.

American brand Coach, for example, reported 40% growth in China in 2013 having positioned itself in this category. According to a QQ Finance6 analysis of Chinese media, Coach is successfully pitching itself as a brand that many Chinese consumers either use themselves or buy for family and friends. It doesn’t hurt that compared to many European brands, Coach products are usually 40-60% cheaper.

“The Premium market, with premium referring to ‘affordable luxury’, is where the big numbers are going to be.”

Fuelled by such growth, Coach is likely to continue expanding beyond its 49 stores in China and focus on opening in second and third tier Chinese cities.

The affordable luxury sector in China is also witnessing the emergence of new indie labels7 targeting a number of specific niche crowds. This is positive news for British designers and brands who would otherwise struggle to compete on the same level as major international brands. This shift in customer preference represents huge opportunities for British brands, whether they are fashion designers in London or whisky distilleries in the Lake District. Multi-brand boutiques or lifestyle stores also offer a perfect match for these smaller, niche outlets.

Furla, an Italian accessories brand that targets the affordable luxury market, is already exploiting these opportunities. In a recent interview,8 the company’s CEO, Eraldo Potello, said: “The Premium market, with premium referring to ‘affordable luxury’, is where the big numbers are going to be. It’s not just because the Government is discouraging extravagant spending. People tend to want value for money and great, authentic products at affordable price points.”

Exclusivity VS Accessibility

One of the challenges faced by luxury brands in China is in finding the perfect position between exclusivity and accessibility.

Whereas brands such as Coach have found it profitable to operate within the ‘affordable luxury’ bracket, some brands have taken the decision to define themselves at the other end of the scale.

One such example is luxury travel agent, Affinity China, which provides unique travel experiences for wealthy Chinese. Dubbed by Forbes as ‘post-luxury luxury’ and Marketing Magazine as ‘extreme luxury’, Affinity China and similar brands are aiming at the exclusive elite.

As the Chinese luxury market gets more sophisticated, opportunities for brands that have a truly unique brand proposition can only increase.

Monaco, one of the favourite holiday destinations for the Chinese super wealthy.

Embracing Pop-up

Decades of economic boom have meant that the cost of bricks and mortar is becoming prohibitively high for many new brands targeting tier one and tier two Chinese cities.

Despite huge financial commitments, brands entering China still face barriers when it comes to understanding politics, liaising with landlords, and responding to regional differences in customer preferences and marketing channels. This makes it far more difficult to open a retail store than it was just a few years ago.

Many forward thinking brands and retailers are embracing new ways of launching their brands in China.

One of the most successful examples is British fashion retailer Topshop, who experimented with a single outlet in Shenzhen before opening 30 pop-up stores all over China.9 If you understand the notoriously disparate Chinese market, you’ll understand that’s a smart move.

On any given day, it can be snowing in northern China, whilst people in the south might be wearing a short-sleeved shirt. Tastes, sizes and buying habits all vary enormously across China, with no two provinces behaving the same.

Topshop’s pop-up strategy allowed them to gain a clear understanding of customer needs before making a bricks and mortar investment. It also enabled the brand to establish relationships with landlords, press and media, whilst reinforcing Topshop’s style driven image – a highly appealing proposition for Chinese consumers.

The pop-up approach also works well for luxury brands who want to launch limited edition capsule collections. Fashion house Dior promoted Raf Simon’s first collection through a pop-up store, which opened for just one month in Beijing.

Brands operating in China are already familiar with running exhibitions or promotions in shopping malls, as this offers an excellent way to connect with real customers. With the right planning, it can be an extremely cost effective way to launch or test a brand in China.

Engage Digitally

November 11 is ‘Singles’ Day’ in China – a day of celebration for all people who are single. In 2013, Taobao and Tmall, two of China’s most popular e-commerce platforms, took 5.75 billion USD10 of sales on this day.

The huge potential of e-commerce platforms is forcing all brands, luxury or not, to invest in their digital strategy.

Coupled with this, the next generation of luxury consumers11 typically defined as the ‘post-90s’ demographic, have grown up with mobile. As a result, it’s little surprise that buying online is becoming the norm in China.

Burberry’s comprehensive digital strategy12 combining social, e-commerce and content marketing, is cited as a prime example for other brands: having resulted in a 70% increase in traffic to their website and 400,000 fans on Weibo.

Relationship With Customers

Chinese consumers are well known for being less tolerant of mistakes from western brands than Chinese brands. That is why developing a good relationship with consumers is vitally important for all brands looking to tap into the Chinese market.

After a hiccup in customer service last year, Apple’s CEO issued a direct apology to Chinese consumers whilst in 2012, the boss of French boutique hotel Zadig and Voltaire (by the fashion label Zadig and Voltaire) was forced to apologise after saying that they intended to ban Chinese tourists. In both instances, the sentiments went viral via social media with both the public and influential bloggers recommending a boycott of each brand.

Developing a good relationship with Chinese consumers is not dissimilar to the relationship a brand would seek to develop in any other country. The most important thing to remember is to treat customers well, treat them with respect and make them feel special.

Conclusion

2014 will see China’s luxury sector enter a new era. As Chinese consumers become more sophisticated, their desire for stand-out brands across different price points will only increase.

The slowdown in growth has already created winners like Coach or Furla, but for new brands targeting China this is a very interesting time to enter the market.

There is no denying China’s competitiveness, but the potential in many second and third tier cities remains largely untapped. New brands should learn from the experiences of key international brands who have entered the Chinese market in the last decade. There are many great examples of brands that have successfully launched in China, but similarly there many examples of brands that have been less than successful in their approaches.

The Chinese market is definitely hungry for the right proposition – is your brand ready for it in 2014?

“As Chinese consumers become more sophisticated, their desire for stand-out brands across different price points will only increase.”

To see how UKC Company can help you reach China, please contact our China team [email protected]

Share this article via

References

- Want China Times – Foreign Luxury Brands Desert Shanghai’s Bund as Glamor Fades

- Hurun Report – Hurun Report Chinese Luxury Consumer Survey 2014

- Financial Times – UK Visa Rules Deter Chinese Shoppers

- Daily Mail – China starts televising the sunrise on giant TV screens because Beijing is so clouded in smog

- The Guardian – Baby Milk Powder Rationing Introduced by Supermarkets

- QQ Finance – 奢侈品在中国大衰退:最容易赚钱时代已过去

- Jing Daily – 3 Trends That Show it’s the Right Time for Indie Labels in China

- South China Morning Post – Furla weaves China dream amid affordable luxury boom

- South China Morning Post – Topshop sets sights on ‘pop-up’ campaign

- Bloomberg – Alibaba Breaks Sales Record Amid China Singles-Day Rebate

- UKC Company – The Young Yuan

- Jing Daily – What Burberry Is Doing Right In China